WeWork is one of the world’s most recognizable coworking brands, known for its innovative business model that offers flexible office spaces for businesses of all sizes. As of 2024, the WeWork business model enables operations in 779 locations across 39 countries, managing a total workspace area of 43.9 million square feet.

Most of this space—around 18.3 million square feet—is in the U.S. and Canada. With a membership base of 547,000 users and an average lease commitment of 19 months, WeWork continues to cater to freelancers, startups, and large companies alike.

The $47 Billion Dream Turned Chapter 11 Reality

WeWork started with a big vision and an even bigger valuation. By 2019, it had reached a staggering $47 billion valuation, making it one of the most valuable startups of its time. But cracks in the foundation quickly appeared.

The company’s failed IPO, triggered by concerns over governance and financial losses, marked the beginning of its downward spiral. After years of financial struggles and unfulfilled promises, WeWork filed for Chapter 11 bankruptcy in November 2023.

Post-Chapter 11

Now, WeWork is in a phase of restructuring. The company has downsized significantly, cutting non-essential locations and renegotiating leases to stay afloat. While its future remains uncertain, WeWork is focused on simplifying its operations and finding a sustainable way to remain relevant in the coworking industry.

Why Analyze WeWork’s Business Model?

Understanding the Coworking Industry

The coworking industry has grown significantly in the past decade, fueled by shifts toward flexible work arrangements and remote work. Companies like WeWork have played a major role in shaping this trend. By looking at how WeWork operated—and where it stumbled—we can learn valuable lessons about the industry’s potential and pitfalls.

Lessons from WeWork’s Journey

WeWork’s story isn’t just about coworking spaces. It’s about ambition, mismanagement, and the dangers of prioritizing growth over sustainability. For businesses, investors, and entrepreneurs, understanding WeWork’s rise and fall offers a roadmap of what to do—and what to avoid.

What is WeWork’s Business Model?

Core Offerings

1. Physical Coworking Spaces

- At its heart, WeWork provides coworking spaces. These include shared desks, private offices, and even full-floor office setups tailored to business needs. They’re designed to offer flexibility, community, and convenience.

2. Virtual Shared Spaces and Services

- Beyond physical spaces, WeWork offers virtual services like online collaboration tools, business addresses, and access to networking events. These services cater to remote workers and companies looking for non-traditional workspace solutions.

Revenue Generation Model

1. Leasing and Subletting

- WeWork’s business model revolves around securing long-term leases for large commercial properties in high-demand areas. These spaces are then subdivided into smaller units, which are rented out to members on shorter-term contracts.

- This creates a revenue stream for the company through subletting, although it also exposes WeWork to risks related to the real estate market and economic downturns.

2. Membership Plans and Flexible Solutions

- WeWork generates revenue by offering various membership plans that allow businesses to rent desks, private offices, or entire floors. These memberships are typically more flexible than traditional office leases, with options to scale up or down based on the company’s needs.

- WeWork also offers customized office solutions for larger clients, including enterprise solutions and dedicated spaces tailored to specific business requirements.

Operational Scale

1. Footprint in 2024

- In 2024, WeWork manages 779 locations spanning 39 countries, with 18.3 million square feet situated in the United States and Canada. The company’s international presence spans key global markets, including Europe, Asia, and Latin America.

2. Membership Base

- WeWork’s network serves 547,000 members, ranging from solo entrepreneurs to large corporations. The average commitment term for members is 19 months, which reflects a mix of short-term flexibility and medium-term stability.

3. Market Focus

- The U.S. and Canada remain the largest markets for WeWork, contributing significantly to the company’s overall revenue. Despite its international footprint, the company continues to focus heavily on its North American operations.

4. Commitment Terms

- WeWork’s customers typically commit to membership terms of about 19 months on average. This gives members the flexibility to adjust their workspace needs while ensuring some level of stability for WeWork’s revenue stream.

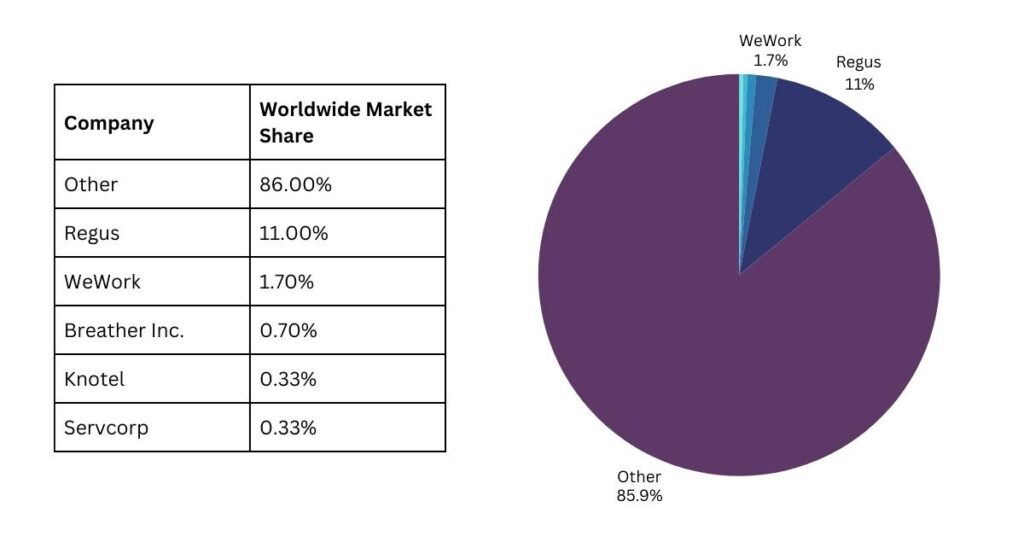

Market Share of WeWork

WeWork is still one of the largest players in the coworking industry, despite its recent struggles. As of 2024:

- WeWork accounts for approximately 20% of the global coworking market, making it a leader in the industry.

- The U.S. and Canada represent its largest markets, with 18.3 million square feet of operational space.

- Its membership base of 547,000 is diverse, including freelancers, small businesses, and large corporations.

Competitors like IWG have more locations globally but lack the aggressive branding and innovative image that WeWork maintains. Meanwhile, smaller players chip away at WeWork’s market share with niche solutions and lower costs.

How Does WeWork Earn Money? (Revenue Model)

WeWork’s revenue model is primarily based on leasing large commercial spaces and converting them into smaller, flexible office units that it rents out to individuals and companies.

Key Revenue Streams:

1. Membership Fees:

- Freelancers and businesses pay monthly fees for access to shared workspaces, private offices, or customized setups.

- Plans are highly flexible, ranging from daily hot desks to multi-year agreements.

2. Custom Office Solutions:

- Larger corporations can lease entire floors or customized office spaces for their teams. These deals often involve long-term commitments.

3. Event and Meeting Spaces:

- WeWork rents out its event venues and meeting rooms to members and non-members for a fee.

4. Virtual Services:

- Services like virtual business addresses, mail handling, and access to online collaboration tools also contribute to revenue.

5. Partnerships and Upselling:

- Partnerships with service providers (e.g., insurance, software tools) generate additional income.

- Upselling premium services like priority support or exclusive access to facilities boosts revenue.

Challenges in the Revenue Model:

Fixed Lease Costs:

- WeWork signs long-term leases with landlords but offers short-term agreements to tenants, which can create financial mismatches during downturns.

Dependence on Occupancy Rates:

- The profitability of a location depends on achieving high occupancy, which can fluctuate based on market demand.

Despite these challenges, the WeWork business model has been instrumental in popularizing flexible office spaces globally and remains a blueprint for many competitors.

Read More: BookMyShow Success Story : India’s Entertainment Ticketing Giant

Is WeWork Truly a Tech Company?

Technology Integration in Operations

WeWork integrates various technologies to enhance how its spaces function. For example, it uses IoT (Internet of Things) devices to monitor workspace usage. These devices track metrics like conference room availability, energy consumption, and even foot traffic. This data helps WeWork optimize layouts and energy usage, making workspaces more efficient.

On top of that, the company relies on data-driven insights to design offices that fit customer needs better. For instance, analytics can highlight which areas are overused or underutilized, enabling changes that improve functionality and profitability.

Tech-Driven Differentiation

WeWork uses technology to set itself apart from traditional real estate companies. It offers seamless digital solutions, such as mobile apps that let members book desks, reserve meeting rooms, or manage billing. These small conveniences create a modern, user-friendly experience that appeals to its tech-savvy customer base.

Compared to older real estate models, WeWork’s focus on automation and connectivity allows it to claim a level of innovation that competitors like Regus or IWG don’t emphasize as heavily. This tech-first branding plays a big role in attracting investors and customers, especially in the early years.

Criticism of the “Tech” Label

Despite these advancements, many argue that WeWork isn’t truly a tech company. Its primary business—leasing and subletting office spaces—is rooted in real estate, not technology. Critics believe the tech label was more of a marketing strategy to inflate its valuation.

Traditional real estate firms like Regus and IWG have similar business models but don’t promote themselves as tech companies. Unlike WeWork, they focus on steady profits rather than rapid, tech-style growth. This raises questions about whether WeWork’s emphasis on technology was justified or merely a way to stand out in a crowded market.

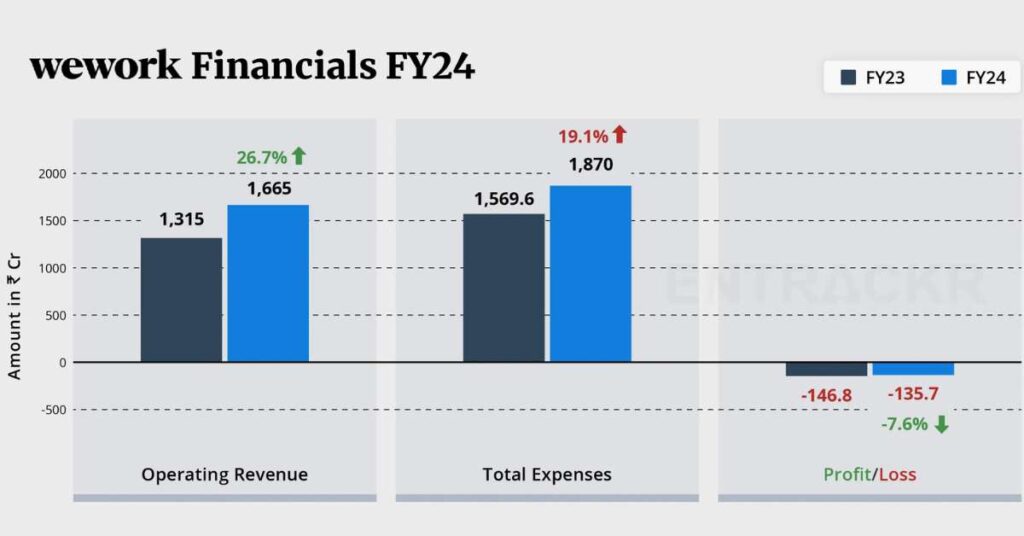

WeWork Revenue and Profit

WeWork, a global leader in flexible workspace solutions, has experienced significant revenue growth but also faced challenges in its profitability over the years. As of 2024, here’s a detailed look at its revenue model and financial performance.

Sure! Here’s a summary of WeWork’s revenue and profit in a table format:

| Category | FY23 | FY24 | Change (%) |

|---|---|---|---|

| Total Revenue | Rs 1,315 crore | Rs 1,737 crore | +32.0% |

| Membership Revenue | Rs 941.6 crore | Rs 1,402.5 crore | +48.9% |

| Revenue from Additional Services | Rs 373.4 crore | Rs 254.5 crore | -31.7% |

| Non-Operating Income (Interest & Gains) | Rs 0 | Rs 72 crore | N/A |

| Total Expenses | Rs 1,569.6 crore | Rs 1,870 crore | +19.1% |

| Depreciation & Amortization | Rs 637 crore | Rs 744 crore | +16.9% |

| Finance Costs | Rs 413.7 crore | Rs 507.7 crore | +22.6% |

| Operating Loss | Rs 146.8 crore | Rs 135.7 crore | -7.6% |

| EBITDA | Rs 1,024 crore | Rs 1,119 crore | +9.3% |

| EBITDA Margin | 61.5% | 64.42% | +2.92% |

| Operating Cash Flow | Rs 1,034 crore | Rs 1,160 crore | +12.2% |

Revenue Generation Model

WeWork’s primary source of revenue comes from the leasing of flexible office spaces. The company rents out these spaces to individuals, small businesses, and large enterprises through various membership plans. These plans include access to shared workspaces, private offices, meeting rooms, and additional services like internet access, printing, and event spaces.

- Membership Revenue: The largest contributor to WeWork’s revenue is membership fees. These include flexible desk options, private office spaces, and custom office solutions. Membership revenue in FY24 accounted for 84% of the total operating revenue. WeWork saw a substantial increase of 48.9% in membership revenue in FY24, totaling Rs 1,402.5 crore.

- Additional Services: WeWork also generates revenue through value-added services. These include renting conference rooms, parking fees, printing charges, and other administrative services. However, revenue from these services declined by 31.7% during FY24.

- Non-Operating Income: Apart from operational revenue, WeWork earned around Rs 72 crore from non-operating income, including interest and gains from financial assets. This brought the overall revenue to Rs 1,737 crore in FY24.

Profitability and Losses

Despite a strong revenue stream, WeWork has faced financial difficulties, particularly in terms of profitability.

- Total Expenses: WeWork’s total expenses for FY24 were Rs 1,870 crore, marking a 19.1% increase compared to the previous fiscal year. The largest contributor to these costs was depreciation and amortization, which accounted for 40% of the total costs and increased by 16.9% to Rs 744 crore. Finance costs also rose significantly, increasing by 22.6% to Rs 507.7 crore.

- Losses: Despite the revenue growth, WeWork reported a loss of Rs 135.7 crore in FY24, a reduction from the Rs 146.8 crore loss in FY23. The decline in losses indicates some improvement in financial performance, though the company is still grappling with its path to profitability.

- EBITDA: WeWork managed to achieve an EBITDA of Rs 1,119 crore in FY24, reflecting the company’s improved operational efficiency. Its EBITDA margin also improved to 64.42%, signaling better cost management.

- Operating Cash Flow: WeWork reported a positive operating cash flow of Rs 1,160 crore in FY24, demonstrating its ability to generate cash from its core operations despite ongoing losses.

Financial Restructuring and Bankruptcy Impact

In November 2023, WeWork filed for Chapter 11 bankruptcy protection in the US, largely due to mounting debt and operational inefficiencies. However, the company emerged from bankruptcy in May 2024, following restructuring efforts. Despite this setback, WeWork’s Indian operations (WeWork India) have remained a strong player in the market and are now aiming for an IPO with a valuation of $2-2.5 billion.

Source: Entrackr

Risks and Challenges in the WeWork Business Model

Financial Risks

One of the biggest risks in WeWork’s business model is the mismatch between its long-term lease obligations and short-term sublets. The company commits to paying landlords fixed amounts for years, but its customers can cancel much sooner. If demand falls, WeWork is stuck with hefty bills and empty offices.

WeWork’s success also depends on rising real estate prices. The idea is to lock in leases at lower rates and profit as market rates climb. But in a downturn, this strategy backfires, forcing the company to lose money on underpriced subleases.

Economic Sensitivity

WeWork relies heavily on freelancers, startups, and small businesses—groups that are especially vulnerable during economic slowdowns. These customers are often the first to cut expenses when times get tough, leaving WeWork with fewer members and more empty desks.

This overreliance on high-risk tenants creates instability. When the economy struggles, so does WeWork, making it harder to maintain cash flow and meet financial commitments.

Brand and Market Challenges

The bankruptcy filing in 2023 severely hurt WeWork’s reputation. For many businesses, trust is key when choosing a coworking provider. Bankruptcy raised doubts about WeWork’s ability to meet its obligations, which could deter potential members.

On top of that, WeWork faces tough competition from smaller, more profitable coworking firms. These competitors often operate with leaner models, focusing on specific niches or local markets. Unlike WeWork, they don’t rely on global expansion or risky financial practices, giving them a more stable footing.

Read More: OfBusiness Business Model: From Procurement to Profit

Competitive Landscape

The coworking industry has grown rapidly in the past decade, attracting multiple players who compete for market dominance. WeWork, despite its challenges, remains a well-known brand in this space. Key competitors include:

- IWG (formerly Regus): Known for its stable operations and profitability, IWG is WeWork’s largest competitor, offering coworking solutions in over 120 countries.

- Spaces: A subsidiary of IWG that targets creative professionals and startups, competing directly with WeWork’s modern aesthetic and flexible offerings.

- Local and Niche Players: Many regional coworking spaces cater to specific markets, offering competitive pricing or niche services like women-only coworking or eco-friendly spaces.

- Big Tech and Corporates: Companies like Google, Amazon, and even traditional landlords now offer flexible workspace options to compete with coworking firms.

Competitive Advantages of WeWork:

WeWork differentiates itself with its scale, branding, and user-friendly technology integration, offering flexible spaces tailored to both startups and Fortune 500 companies. However, it faces criticism for financial instability and heavy reliance on long-term lease agreements.

The Rise and Fall: Lessons from WeWork’s History

The IPO Failure in 2019

In 2019, WeWork was poised to go public with a highly anticipated IPO. But instead of being a triumphant moment, it turned into a disaster. When the company released its public prospectus (S-1 filing), investors raised alarms about its governance, business model, and mounting losses. The scrutiny quickly snowballed.

Adam Neumann, WeWork’s charismatic but controversial CEO, became a focal point of criticism. He was accused of mismanagement, extravagant spending, and creating a company culture that valued hype over substance. By September 2019, Neumann stepped down as CEO and relinquished his majority voting control. WeWork’s IPO was formally withdrawn, and its valuation plummeted from $47 billion to roughly $10 billion almost overnight.

SoftBank’s Role

SoftBank, one of WeWork’s largest investors, played a major role in both its rise and attempted recovery. The Japanese conglomerate had poured billions into WeWork, betting big on its potential to dominate the coworking industry. However, this financial backing also encouraged rapid, unsustainable growth.

After the IPO failure, SoftBank stepped in to bail out WeWork. It provided $1.7 billion to buy out Adam Neumann and took control of the company’s board. SoftBank’s strategy shifted from aggressive expansion to damage control, aiming to stabilize WeWork and reduce its financial bleeding.

The 2023 Bankruptcy

Despite SoftBank’s efforts, WeWork’s struggles didn’t end. Years of high lease obligations, coupled with the shift to remote work during the pandemic, drained its finances. By August 2023, the company warned investors that it might not survive.

In November 2023, WeWork officially filed for Chapter 11 bankruptcy. Its market capitalization had plunged to just $21 million, a stark contrast to its $47 billion peak. The bankruptcy marked the end of an era for WeWork, turning it into a cautionary tale about overvaluation and unchecked growth.

Post-Bankruptcy: What’s Next for WeWork?

Current Restructuring Plans

Post-bankruptcy, WeWork is focused on survival. The company has downsized significantly, cutting underperforming locations and renegotiating lease terms to lower costs. It’s shifting gears, aiming for a leaner operation that prioritizes profitability over expansion.

There’s also speculation that WeWork might explore new business strategies, such as focusing more on virtual offerings or partnering with real estate firms to reduce risk. However, these plans are still unfolding, and their success remains uncertain.

Industry Outlook in 2024

The coworking industry is evolving rapidly. Trends like hybrid work and the demand for flexible office spaces are creating new opportunities. Companies are looking for scalable solutions that allow them to adapt to fluctuating employee needs, which could work in WeWork’s favor if it manages to regain trust.

That said, competition is fiercer than ever. Smaller, more profitable operators are thriving by offering tailored coworking experiences without the baggage of global expansion.

Potential Pathways for Revival

For WeWork to stage a comeback, it needs to rethink its priorities. The focus must shift from hypergrowth to sustainable profitability. This could mean scaling back operations further and zeroing in on core markets like the U.S. and Canada.

Another potential pathway is through partnerships and innovation. By collaborating with property owners or offering tech-driven solutions for hybrid work, WeWork could carve out a niche in the coworking space. The key will be balancing ambition with financial discipline—a lesson learned the hard way.

Conclusion

WeWork’s story is a case study in what happens when growth takes precedence over sustainability. From its meteoric rise to its dramatic fall, the company highlights the risks of poor governance and over-reliance on investor hype. Leadership matters, and so does a solid business model.

Today, WeWork is at a crossroads. Its bankruptcy and restructuring efforts may give it a second chance, but the road ahead is anything but certain. Whether WeWork can successfully pivot and rebuild its reputation remains to be seen.

For now, WeWork serves as both a cautionary tale and a source of valuable lessons—for startups, investors, and the coworking industry alike. The question is: Will WeWork’s story end as a successful turnaround or a lasting warning of ambition gone wrong?

Source: Wikipedia, managementstudyguide, investopedia, growthx, startuptalky, entrackr and etc.

FAQs

What Kind of Company Is WeWork?

WeWork is a coworking space provider operating globally. It’s not a traditional real estate firm because it emphasizes flexibility, community, and services aimed at enhancing user experiences.

What Type of Company Is WeWork?

WeWork is a real estate-focused company with a tech-enabled service layer. While it positions itself as a technology-driven workspace provider, its core operations revolve around real estate leasing and management.

What Services Does It Offer?

WeWork is in the coworking and flexible workspace industry, providing:

Physical Spaces: Shared desks, private offices, and enterprise-grade spaces.

Virtual Services: Business addresses, virtual mail handling, and collaboration tools.

Amenities: High-speed internet, conference rooms, kitchens, and community events.

What Is WeWork Company Culture?

WeWork’s culture was originally built around:

Community: Designing spaces that encourage collaboration and networking.

Innovation: Adopting technology to enhance workspace experiences.

Entrepreneurial Spirit: Empowering startups and freelancers. However, after its public controversies and bankruptcy, its culture now emphasizes accountability, sustainability, and operational efficiency.

What is WeWork Company Valuation?

WeWork reached a peak valuation of $47 billion in 2019. After its failed IPO, the valuation fell dramatically, eventually plunging to $21 million by late 2023, before the bankruptcy filing.

What Is WeWork’s Business Model?

WeWork operates a real estate arbitrage model with a focus on flexible office spaces:

Leasing & Subletting: The company signs long-term leases for large commercial spaces.

Revenue Generation: Income comes from membership plans, renting workstations, virtual services, and add-ons like meeting room bookings or event hosting.

Target Audience: It serves freelancers, startups, and larger companies seeking adaptable office solutions without committing to traditional long-term leases.

1 thought on “WeWork Business Model – Startup Case Study”